Get answers like this one, first.

Google’s AI Overviews now favor the sources you choose. Add ClearPoint once, and our research shows up in your AI answers — badged and prioritized.

Add ClearPoint as a Preferred SourceFree · one click · applies only to your own Google results.

GASB 103 is the first major overhaul of government financial reporting since 1999. Here's what local governments must do before June 30, 2026.

The Biggest Government Reporting Overhaul in 25 Years Is Here

June 30, 2026. That's the first reporting deadline for GASB Statement No. 103 — the first significant restructuring of the government financial reporting model since GASB Statement No. 34 was issued in 1999. Technically, the standard is effective for fiscal years beginning after June 15, 2025, which means the earliest-affected governments are those with a June 30 fiscal year end.

For finance and strategy teams at state and local governments, this is not a minor technical update. GASB 103 fundamentally changes how you structure your Management Discussion & Analysis, how you present financial accountability to the public, and how you demonstrate the analytical depth behind your government's financial results.

If your reporting cycle ends June 30, you have roughly 14 weeks from today. If it ends September 30 or December 31, you have slightly more — but the planning and restructuring work needs to start now.

This article breaks down exactly what GASB 103 requires, what it means for your team operationally, and how governments are approaching the transition without rebuilding everything from scratch.

What Is GASB Statement No. 103?

GASB Statement No. 103, Financial Reporting Model Improvements, is the Governmental Accounting Standards Board's comprehensive update to the framework established by GASB 34 in 1999. That original framework created the modern structure of government financial statements — including the government-wide statements, fund-level statements, and the Management Discussion & Analysis section that finance officers know well.

Twenty-five years later, GASB 103 is the first major revision to that model. Its stated goal is to improve the effectiveness of financial reporting — specifically, to make government financial statements more useful for decision-making and accountability assessment.

Effective date: Fiscal years beginning after June 15, 2025, and all reporting periods thereafter — meaning the first affected fiscal year ends June 30, 2026 for governments on a standard July–June cycle. (GASB Statement No. 103)

Who it affects: All state and local governments that produce GAAP-compliant financial statements — approximately 90,837 governmental entities across the United States, according to the U.S. Census Bureau's 2022 Census of Governments, from large cities and counties to special districts, transit authorities, and school systems.

Key Changes Under GASB 103

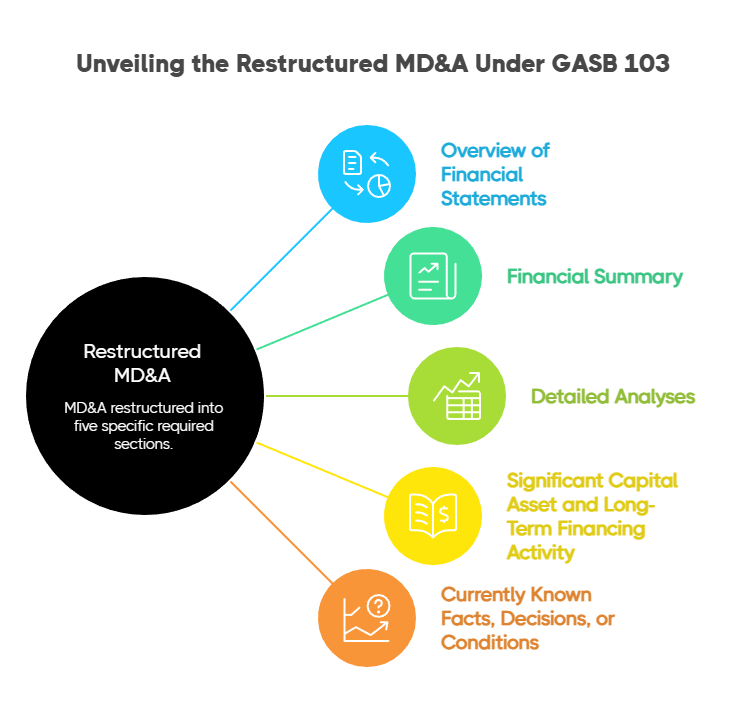

1. Restructured Management Discussion & Analysis (MD&A)

The MD&A section is where governments explain their financial position in plain language for elected officials, residents, and oversight bodies. GASB 103 restructures the MD&A into five specific required sections (Baker Tilly):

- Overview of the Financial Statements — explaining the relationships between the statements

- Financial Summary — a high-level narrative of key financial results

- Detailed Analyses — explaining why results changed from the prior year, not just by how much

- Significant Capital Asset and Long-Term Financing Activity — capital and debt activity during the year

- Currently Known Facts, Decisions, or Conditions — forward-looking information expected to affect future results

GASB 103 explicitly prohibits boilerplate language — the MD&A must provide substantive analysis, not just restate the numbers. Finance teams will need to rebuild their templates around these five sections.

2. Updated Government-Wide Financial Statement Requirements

GASB 103 modifies the requirements for government-wide and fund financial statements — the core financial documents that present a government's overall fiscal health. Changes affect how certain items are classified, presented, and disclosed.

3. Replacement of Extraordinary/Special Items with Unusual and Infrequent Items

GASB 103 eliminates the categories of "extraordinary items" and "special items" — concepts inherited from private-sector accounting — and replaces them with a single concept: unusual and infrequent items. These must be displayed separately in government-wide, governmental fund, and proprietary fund statements of resource flows, presented as the last items before the net change in resource flows. This simplification improves comparability across governments and removes classification ambiguity that has historically created audit risk.

4. Proposed Implementation Guidance

As of February 2026, GASB is also seeking public comment on a proposed Implementation Guide that will provide question-and-answer guidance on GASB 103's requirements — indicating that detailed compliance questions are still being resolved in real time.

How GASB 103 Impacts Local Government Operations

Understanding the technical requirements is step one. Understanding the operational implications — what your team actually has to do differently — is where the real preparation begins.

Impact 1: Your MD&A Structure Needs a Rebuild

Before GASB 103: Most governments have MD&A templates built around GASB 34's 1999 structure — sections inherited from prior years, slightly updated each cycle, rarely questioned.

After GASB 103: That template is no longer compliant. Finance teams must restructure the MD&A to align with the new five-section framework, which means rethinking the narrative flow, the data inputs, and the linkage between financial and operational information.

For teams that produce their MD&A manually — pulling data from multiple systems into a Word document — this restructuring is a significant lift. The risk of error rises, and the timeline is short.

Impact 2: Your MD&A Must Explain "Why" — Not Just "What"

Before GASB 103: Most MD&As were built around presenting numbers — fund balances, revenue comparisons, expenditure variances — with a brief narrative that typically said little more than "revenues increased by X%." Boilerplate language was common, with minimal year-over-year differences in the actual prose.

After GASB 103: The standard explicitly prohibits that approach. The new Detailed Analyses section requires finance teams to explain why results changed — what decisions, conditions, or events drove the numbers. Governments that lack organized, current performance data will struggle to write compliant, substantive MD&A narratives under deadline pressure.

Impact 3: Audit Risk Increases During the Transition Year

The first year of compliance with any new GASB standard is always the highest-risk year. Auditors will be scrutinizing compliance with the new structure, and errors in MD&A presentation or financial statement classification can trigger findings.

Finance teams that try to retrofit their old reporting structures — adding new sections to a legacy template — face the highest audit risk. Teams that build a clean, standard-compliant framework from the ground up face a higher upfront workload but lower long-term risk.

Impact 4: Council and Public Communication Expectations Rise

The accountability transparency that GASB 103 demands isn't just an audit checkbox. It's what elected officials and residents increasingly expect from local government. Governments that produce clear, decision-useful financial reporting build public trust. Those that produce opaque or boilerplate reporting face growing scrutiny.

A 5-Step Action Plan for GASB 103 Compliance

Here's how finance and strategy teams should approach the next 14–24 weeks.

Step 1: Map the Gaps Between Your Current MD&A and GASB 103 Requirements

Start with an honest assessment. Pull your most recent MD&A and work through GASB 103's new five-section structure. Where does your current narrative structure align? Where does it fall short? Which sections are missing entirely? Where does the narrative restate numbers rather than explain them?

This gap analysis is the foundation for everything that follows. Without it, you're rebuilding without a blueprint.

Step 2: Organize Your Analytical Data Before You Write a Word

GASB 103's new Detailed Analyses section requires explanations of why results changed — not just by how much. That means you need clean, current data on departmental performance, budget variances, and the decisions behind them before you can write a compliant MD&A narrative. If that data lives in disconnected spreadsheets or siloed department reports, assembling it under deadline pressure creates real risk.

The governments that handle this most effectively are those that have already organized their performance data in a structured, accessible system. Their finance teams aren't chasing information in the final weeks — they're writing analysis.

Step 3: Build (or Adopt) a Compliant MD&A Template — Now

Don't wait until June to redesign your MD&A. Build the new structure now, get it reviewed by your auditors, and test it against your data before your fiscal year closes. A template built in March is significantly better than a template built in June.

Organizations like the Government Finance Officers Association (GFOA) are actively developing GASB 103 guidance and resources — consult their materials as part of your template development.

Step 4: Automate the Data Collection You've Been Doing Manually

The single biggest operational risk in GASB 103 compliance is manual data assembly. Every hour your team spends copying numbers from spreadsheets into Word documents is an hour of error risk and a bottleneck that becomes a crisis when deadlines compress.

If your current process relies heavily on manual data gathering for financial reporting, GASB 103 is the right moment to change that. Strategic performance management platforms can automate the collection of performance data, connect it to departmental goals, and generate narrative-ready reporting structures — reducing the workload of MD&A production significantly.

Step 5: Coordinate Finance and Operations Teams Now

GASB 103's analytical requirements mean that your finance team can no longer produce a compliant MD&A in isolation. The new Detailed Analyses section requires explanations grounded in departmental activity — budget decisions, operational results, capital project status — that typically live outside the finance department.

Start the coordination now. Establish clear data-sharing processes with department heads, agree on timelines for information gathering, and build a joint review process for the draft before your fiscal year closes.

How ClearPoint Helps Local Governments Navigate GASB 103

More than 1,200 local governments — including Scottsdale, AZ and Charlotte, NC — use ClearPoint Strategy to manage their strategic plans, track performance measures, and produce the kind of analytically rigorous, decision-useful reporting that GASB 103 now requires.

Here's where ClearPoint specifically addresses GASB 103's challenges:

MD&A Data Assembly: ClearPoint centralizes performance data — departmental goals, measures, milestones, and results — in a single system, eliminating the manual data gathering that creates bottlenecks and errors during reporting cycles. Finance teams can pull structured, auditable data directly into their MD&A narrative without chasing spreadsheets across departments.

Analytical Narrative Support: GASB 103's Detailed Analyses section requires explaining why results changed. ClearPoint's scorecards and reporting dashboards give finance teams the organized, current performance context they need to write substantive analysis — department-by-department — rather than copying language from prior-year reports.

Executive and Public Dashboards: ClearPoint's public-facing dashboards allow governments to surface their performance data for residents and elected officials — supporting the decision-usefulness and transparency goals that GASB 103 was written to advance.

Reporting Automation: Teams that previously spent days assembling MD&A supporting data can use ClearPoint's automated reporting to generate structured performance reports on demand — reducing GASB 103 compliance preparation from weeks to days.

Scottsdale, AZ used ClearPoint to build public performance reporting that makes their strategic outcomes visible to both council and residents — producing the kind of clear, decision-useful reporting that GASB 103's MD&A improvements are designed to achieve.

Don't Retrofit — Rebuild Right

The temptation with every new accounting standard is to do the minimum: add a section here, adjust some language there, and file a compliant report. That approach works once. It doesn't scale, and it creates compounding technical debt that makes every future compliance cycle harder.

GASB 103 is an opportunity to build a reporting infrastructure that actually serves your government's accountability goals — one that produces analytically substantive, auditable MD&As efficiently, year after year.

With roughly 14 weeks until the June 30 reporting deadline, the time to start is now. Not after your fiscal year closes. Not after you've seen what your auditor says. Now.

See how ClearPoint helps local governments build GASB 103-ready reporting frameworks — request a demo today.

Frequently Asked Questions About GASB 103

When does GASB 103 take effect?

GASB Statement No. 103 is effective for fiscal years beginning after June 15, 2025, and all reporting periods thereafter. For governments on a standard July–June fiscal year, this means the first affected reporting year ends June 30, 2026. September 30 and December 31 fiscal year governments follow in subsequent cycles.

Does GASB 103 replace GASB 34?

GASB 103 updates and amends GASB 34 — it is not a full replacement. GASB 34 remains the foundation of the government financial reporting model; GASB 103 is the most significant revision to that foundation since 1999.

What is the biggest operational change required by GASB 103?

For most governments, the biggest change is in the MD&A section — both in its new five-section structure and in the requirement to provide substantive analysis explaining why results changed, rather than simply restating numbers. Finance teams with legacy MD&A templates built around GASB 34's 1999 structure will need to rebuild those templates to comply.

Is GASB 103 mandatory for all local governments?

Any state or local government that prepares GAAP-compliant financial statements must comply with GASB 103 for fiscal years beginning after June 15, 2025.

Where can I find the official GASB 103 guidance?

The full text of GASB Statement No. 103 is available at gasb.org. The proposed Implementation Guide is open for public comment as of early 2026.